What a horrendously bad year for the growth of my stock portfolio in 2022! My stock portfolio increased in value by 84.3k € of which 74.8k € was in savings and a measly 9.5k € came from value increase. Bad, bad, bad! The market crash have had an impact for sure.

In the previous report the stock portfolio development 2021 I spoke about that I had readjusted my target from the original 750k € to 425k €, so that I could buy a renovations object, in ideally the south of France. I want to live close to the beach and I want to be able to go skiing during winter so more places have appeared on the radar as of late and more money is needed to buy the places. I've reached the target (~450k €) and I'm very close to handing in my letter of resignation but in the last weeks they've been pushing that they will increase the age of when one is legally allowed to take out from the private pension scheme from 55 to 57 years of age. This is to follow the 2 year increase in the UK from 65 to 67 years for retirement. Very annoying... So I need to fund a further two years and yes, currently house prices are dropping but not as heavily as I would have liked to see so I can't fund the two years by putting less into the renovation object.

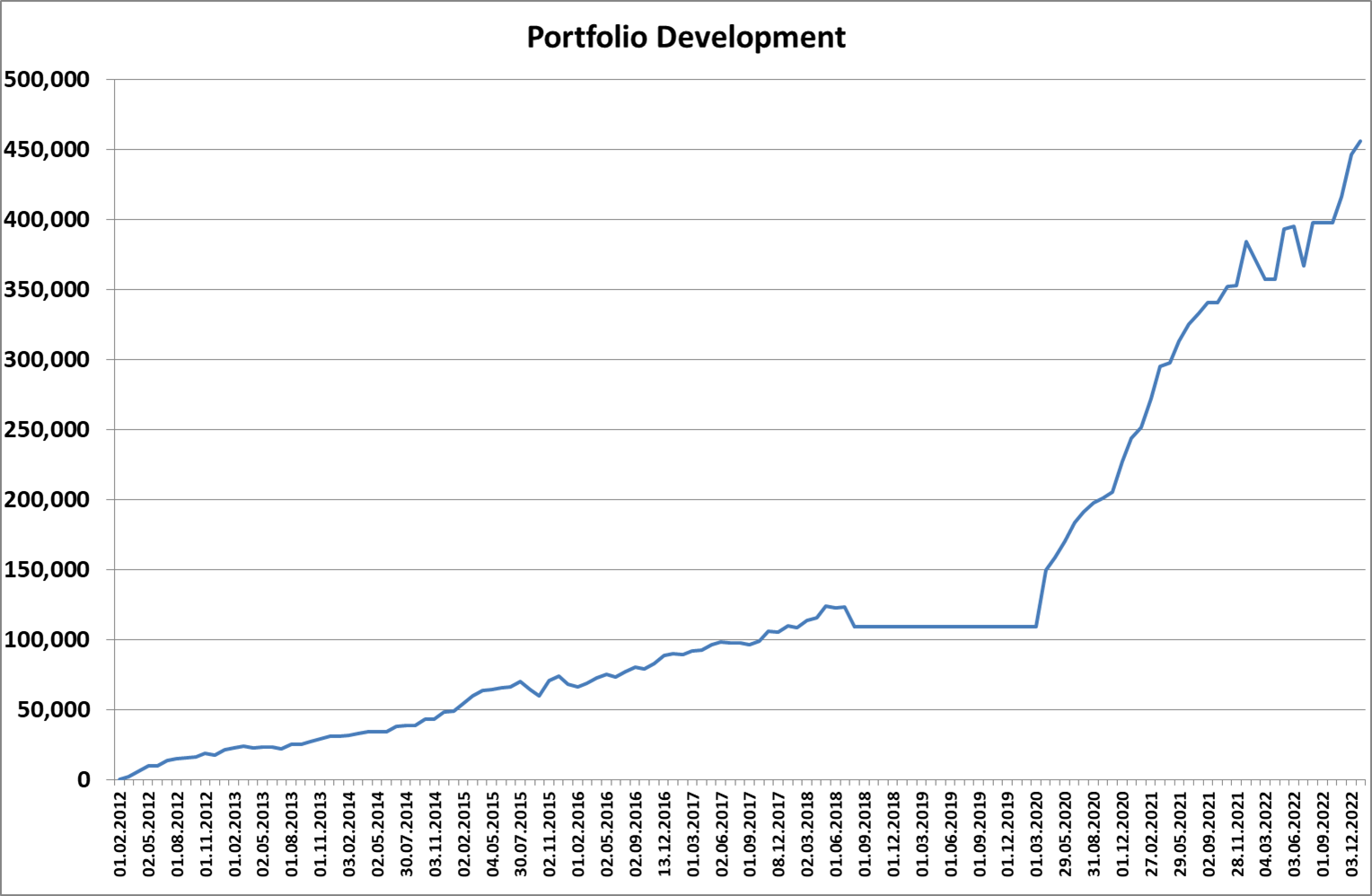

As can be seen in the graph above my plan is working well. In my first year (2012) of investment I ended up with a stock portfolio in the value of 17,659 € which was 4,744 € more then my plan required. In the second year (2013) my stock portfolio grew with 73 % and ended up with a value of 30,623 € which was 4,723 € above my target meaning that I managed to stay ahead of my plan but I did not manage to increase this advantage. In the third year (2014) my stock portfolio grew with 57% and I ended up with a value of 48,208 € which is then 8,333 € ahead of my investment plan which means that I managed to double my advantage during 2014. In the fourth year (2015) my portfolio grew by 53% and I am up at a value of 73,579 €. My plan was to have a stock portfolio of 54,915 € in the end of 2015 which means that I am now 18,664 € ahead of my plan. During my fifth year (2016) which was horrible in terms of new investments my portfolio still grew by 20% and the value was up at 88,414 € which mean that I was still 17,312 € ahead of my plan. In the sixth year (2017) the portfolio grew by 24% with a value of 109,606 € which was 21,802 € ahead of my plan. Followed by my seventh year of investing (2018) and an estimated growth of 19% and a value of ~130,000 which kept me 22,726 € ahead of my plan (hit by divorce). To then in my eighth year of investing (2019) with a growth of 24% with a stock portfolio value of 160,669 € and me being 33,216 € ahead of the plan (still hit by divorce). In the ninth year of investing (2020) and a growth of 52% and a stock portfolio at 243,801 € and me being 94,629 € ahead of the plan (final year of being hit by divorce). In my tenth year (2021) I had a growth of 57% and a stock portfolio at 383,941 € and by that I was 211,395 € ahead of the original plan. In the eleventh year (2022) I had a growth of measly 19% and a stock portfolio of 455,859 € and by that I was 258,156 € ahead of the original plan.

The year was kept on the down and low due to the poor performance of the stock portfolio. Savings were kept up at an extremely high value. It is insane to be able to save almost 75k € per year in the last two years.

Conclusion: 2022 did not become the best year ever. The massive saving ability once again helped my out substantially but the stock portfolio did not perform well at all. At least it did not drop down so I should potentially be pleased about that but I am not.

No comments:

Post a Comment